How’s The Market? Which One?

The first question is fairly common. The second question is quite rare. Why? Because there are numerous stock market indexes and from the narrowest to the broadest there is a huge difference in the stocks included and their returns.

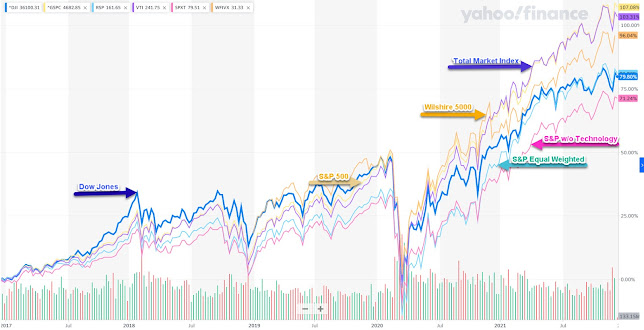

The best-known index is the Dow Jones Industrial Average, which is composed of 30 of the largest U.S. companies. The Dow, like most other indexes, is a biased reflection of market performance. The obvious reason is that it is a small sample, albeit that of the largest companies. Less obvious, but more important, is that the index movements are primarily driven by the higher priced stocks in the group.

Professional investors pay more attention to the Standard & Poor’s 500 Index, the movements of which often vary substantially from those of the Dow. The S&P is weighted by the market value of the companies’ shares, which means that the biggest companies in the group have the greatest impact. In recent years, major technology companies such as Meta (née Facebook), Apple, Amazon, Netflix, and Alphabet (née Google) have been the main engines for gains.

A more accurate portrayal of how the S&P has been doing is seen by viewing the Invesco S&P 500 Equal Weight exchange-traded fund, which equally weights all the companies included, so the changes in the prices of the smallest companies have the same impact as those of the giants.

The ProShares S&P 500 Ex-Technology exchange-traded fund takes this one step further by measuring the S&P 500 without the 70 technology companies that are in the index. That slices off about 30-35% of the aggregate value of the companies covered, but it also shows that the typical returns from most stocks are far lower.

Rather than narrowing, Vanguard’s Total Market Index exchange-traded fund includes a total of 4,124 different stocks. Even broader is the Wilshire 5000 Index Fund, which (no surprise) includes 5,000 stocks.

From

top to bottom, the returns over the latest five years have differed

greatly. The top returns were from the

S&P 500 and the Total Market Index, both of which had a massive tech bias. The lowest returns were from the Dow and the

S&P 500 ETF ex-the tech stocks. The

gains for the latter pair were about one-third lower than for the top two.

So when someone asks you about the market, you need to ask which one.

Sound Asset Management Inc.

Weston, CT 06883

203-222-9370

Any

questions? Please contact me at nrwayne@soundasset.com

Comments

Post a Comment